Deregulating the Canadian dairy supply management system could lose $2.1 billion for the Canadian GDP, states a report commissioned by the Agropur Dairy Cooperative in Quebec.

Conducted by the Boston Consulting Group, the report uses a combination of real-world analysis and hypothesis of future affects in Canada. The paper considers the United States as a supply source for Canada and hypothesizes what deregulation could look like.

It also analyzes the deregulation of dairy markets in other parts of the world, including Australia, New Zealand, the European Union and the United Kingdom. The paper considers the United States as a supply source for Canada and hypothesizes what deregulation would look like.

With U.S. President Donald Trump vehemently advocating the removal of Canada’s dairy supply management as part of NAFTA negotiations, a look into how that would affect Canadian producers is worth considering.

Pressure is also increasing on the Canadian dairy industry and NAFTA negotiations are just one part of that, states the report. Critics of the system state consumers pay too much for dairy products in Canada, the quotas system also makes it difficult for growth and consolidate, and can bring higher debt to farmers.

The report considers the impacts on the dairy industry — in production and processing — in areas where deregulation occurred around the world and how competition from the United States could change things.

—Click HERE to read the full report and hypothesis—

Canada deregulation hypothesis

If Canada were to immediately do away with dairy supply management without government subsidy, the industry could see a net loss of $2.1 to $3.5 billion and could threaten 24,000 jobs.

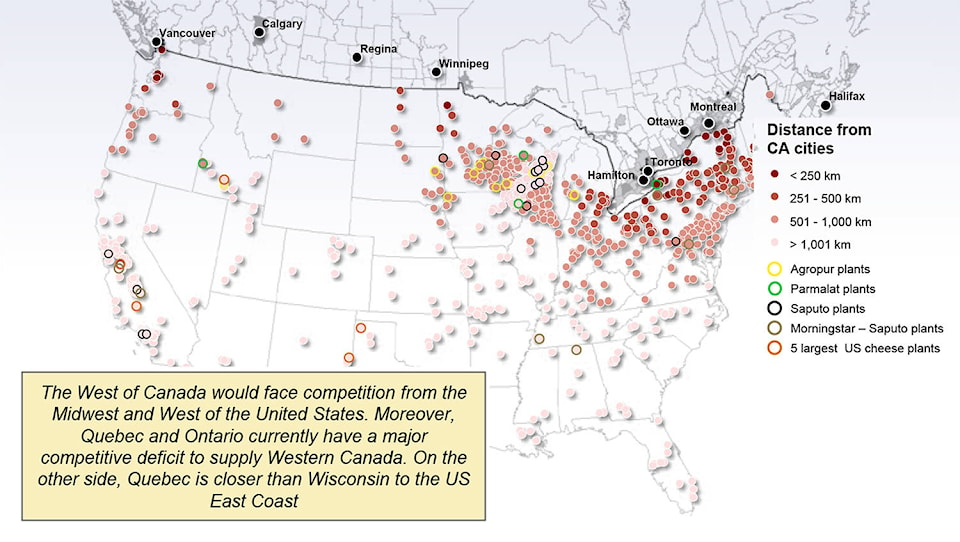

The competitive challenge is mainly caused by the U.S. dairy production’s proximity to the Canadian border.

“One initial observation shows that there are 960,000 milk cows (2015 estimates) based in the United States that are within 250 km of a Canadian dairy plant. This is an equivalent amount to the whole Canadian dairy livestock,” states the report.

Production, yield and dairy farm size is generally higher in the United States, which adds to the challenge Canadian producers would face in competing. Areas such as Quebec would face serious competitive challenges, states the report, however, western Canadian provinces would also face competition from the U.S.

“On the processing side, in the United States there are about 200 milk processing plants within 500 km from Canada and about 500 plants within 1,000 km.”

“Of course, within this same scenario, the remaining producers would then have the opportunity to increase their production,” it states.

Based on the analysis of current markets, and the report’s immediate deregulation hypothesis, 40 per cent of the Canadian dairy industry would be at risk.

“The extent of the risk is unique, because the United States represents a real alternative to supply Canada, with its production 11 times higher and production costs up to 30 per cent lower than in Canada.”

For its hypothesis, the report used these methods:

• Average premium paid in the United States;

• Conversion from pounds to litres;

• Conversion into Canadian dollars with the average exchange rate of US $1 = CA $1.07 over the last 5 years;

• Price difference observed in the north-eastern US States as compared to the average price in the United States;

• Average milk transportation cost (based on 200,000-litre tanks, i.e. the maximum capacity allowed by the US regulation for transportation) for an average distance of 750 km round trip.

Financial repercussions and debt

The debt ratio for Canadian producers is much higher amount than their U.S. counterparts.

In Quebec the average debt per cow is $19,900, and in Ontario it is $16,600 (only Quebec and Ontario were considered in this study). Compared to the U.S., that’s a big difference with northeastern U.S. seeing per cow debt at $3,400 or at the University of Michigan at $4,950.

An immediate deregulation could also hurt the banks.

“Dairy producers are indebted for $16 to $18 billion with Canadian financial institutions, and parts of these loans are at risk,” states the report, adding that lower revenues in a deregulated system might not cover debt serving for farmers.

Deregulation analysis in other countries

With dairy supply management and NAFTA talks under way, a look at how deregulation affected these countries may help understand how Canada would look in non-regulated market.

Australia

The first phase of deregulation in Australia actually saw growth within the industry of four billion litres of milk over a 10 year period, states the paper. However, after the full deregulation Australia saw a seven per cent loss per year from 2000 to 2002.

“The country lost 2,000 farms in two years,” states the report.

What the report finds is that production shifted to southern provinces as costs were lower and climate conditions were more favourable in that area. Australia’s share of the global dairy market dropped to six per cent, down from 18 per cent.

New Zealand

The results in New Zealand paint a far different picture.

After deregulation, the country saw major growth in its production, partly with the amalgamation of the country’s two largest dairy cooperatives.

“New Zealand benefits from exceptional climatic conditions to favour the growth of its dairy production,” states the report. “The abundance of pastures, high rainfall, the absence of extreme cold and heat – basically the temperate climate of the country, are all favourable conditions for milk production.”

New Zealand sees about 32 per cent of global dairy exports.

European Union (EU)

With six countries producing about 70 per cent of milk in the EU — Germany, France, the United Kingdom, Poland, Netherlands and Italy — the report states there are many differences in results.

The removal of guaranteed prices appears to have been replaced by subsidies. The paper points out that in 2013, 57 billion Euros from the Common Agricultural Policy were paid to producers.

A full analysis isn’t available in the report as it was written before the March 2015 full deregulation in the EU, however, the paper does state that several large dairy cooperatives have emerged.

“Our benchmarking shows us that in general, regulated markets seem to create a favourable environment for the emergence of robust milk processors that are leaders in their markets,” states the report.

Indeed, in New Zealand, the large cooperatives have allowed for cost savings to producers and market reach. “This gives a clear advantage to members – milk producers – that benefit…from the output of milk processing.”

United Kingdom

A decrease in production appears to have affected the UK dairy industry despite a one per cent annual quotas increase. Government subsidies have also increased over the years, states the report.

“On the processing side, given their relative weakness as compared to other international players, British processors experienced difficulties in adapting to deregulation, resulting in international processors from other countries in the European Union consolidating the industry.”

Prices for two dairy products — cheese and butter — have increased faster than inflation with relatively high jumps in 2008.

The paper was written by Dominique Benoit for Agropur and Alexandra Corriveau for the Boston Consulting Group, and looks at contributions to the Canadian economy and potential effects of a deregulated system.